Page 1 of 2

RULE-MAKING ORDER

PERMANENT RULE ONLY

CODE REVISER USE ONLY

CR-103P (December 2017)

(Implements RCW 34.05.360)

Agency: Department of Revenue

Effective date of rule:

Permanent Rules

☒ 31 days after filing.

☐ Other (specify) (If less than 31 days after filing, a specific finding under RCW 34.05.380(3) is required and should be

stated below)

Any other findings required by other provisions of law as precondition to adoption or effectiveness of rule?

☐ Yes ☒ No If Yes, explain:

Purpose: This new rule seeks to clarify substantive aspects of the excise tax on capital gains by supplying additional

definitions and examples related to this excise tax.

Citation of rules affected by this order:

New: WAC 458-20-301 – Capital gains excise tax – definitions, deductions, exemptions, and allocation of gains

and losses

Repealed:

Amended:

Suspended:

Statutory authority for adoption: RCW 82.32.300, 82.01.060

Other authority:

PERMANENT RULE (Including Expedited Rule Making)

Adopted under notice filed as WSR 24-06-089 on March 6, 2024 (date).

Describe any changes other than editing from proposed to adopted version: Corrected calculation error in result in

Example 5.

If a preliminary cost-benefit analysis was prepared under RCW 34.05.328, a final cost-benefit analysis is available by

contacting:

Name:

Address:

Phone:

Fax:

TTY:

Email:

Web site:

Other:

Page 2 of 2

Note: If any category is left blank, it will be calculated as zero.

No descriptive text.

Count by whole WAC sections only, from the WAC number through the history note.

A section may be counted in more than one category.

The number of sections adopted in order to comply with:

Federal statute:

New

Amended

Repealed

Federal rules or standards:

New

Amended

Repealed

Recently enacted state statutes:

New

Amended

Repealed

The number of sections adopted at the request of a nongovernmental entity:

New

Amended

Repealed

The number of sections adopted on the agency’s own initiative:

New

1

Amended

Repealed

The number of sections adopted in order to clarify, streamline, or reform agency procedures:

New

1

Amended

Repealed

The number of sections adopted using:

Negotiated rule making:

New

Amended

Repealed

Pilot rule making:

New

Amended

Repealed

Other alternative rule making:

New

Amended

Repealed

Date Adopted: June 28, 2024

Name: Brenton Madison

Title: Rules Coordinator

Signature:

NEW SECTION

WAC 458-20-301 Capital gains excise tax—Definitions, deduc-

tions, exemptions,

and allocation of gains and losses. (1) Introduc-

tion. Beginning January 1, 2022, Washington law imposes an excise tax

on individuals who sell or exchange long-term capital assets. See

chapter 82.87 RCW (capital gains excise tax). This rule provides in-

terpretive guidance related to the tax, including definitions of terms

and explanations regarding the treatment of specific transactions.

This rule contains examples that identify a number of facts, and then

it states a conclusion. The examples are provided only as a general

guide. The tax results of other situations must be determined after a

review of all the facts and circumstances.

(2)

Definitions and terms, and related information.

(a) Adjusted capital

gain. Adjusted capital gain means federal

net long-term capital gain:

(i) Plus, any amount of long-term capital loss from a sale or ex-

change that is exempt from the capital gains excise tax, to the extent

such loss was included in calculating federal net long-term capital

gain;

(ii) Plus, any amount of long-term capital loss from a sale or

exchange that is not allocated to Washington under RCW 82.87.100, to

the extent such loss was included in calculating federal net long-term

capital gain;

(iii) Plus, any amount of loss carryforward from a sale or ex-

change that is not allocated to Washington under RCW 82.87.100, to the

extent such loss was included in calculating federal net long-term

capital gain;

(iv) Less, any amount of long-term capital gain from a sale or

exchange that is not allocated to Washington under RCW 82.87.100, to

the extent such gain was included in calculating federal net long-term

capital gain;

(v) Less, any amount of long-term capital gain from a sale or ex-

change that is exempt under chapter 82.87 RCW, to the extent such gain

was included in calculating federal net long-term capital gain. See

RCW 82.87.020; and

(vi) Plus, any amount of capital loss carryforward from a sale or

exchange that occurred before January 1, 2022, to the extent such loss

was included in calculating federal net long-term capital gain, and

less any long-term capital gain from an installment sale that occurred

before January 1, 2022, to the extent such gain was included in calcu-

lating federal net long-term capital gain. See subsection (3)(a) of

this rule for additional information regarding the two adjustments de-

scribed in this paragraph.

(b)

Another taxing

jurisdiction. Another taxing jurisdiction

means a state of the United States other than the state of Washington,

the District of Columbia, the Commonwealth of Puerto Rico, any terri-

tory or possession of the United States, or any foreign country or po-

litical subdivision of a foreign country. See RCW 82.87.100. The Uni-

ted States is not "another taxing jurisdiction."

(c)

Domicile. In

general, domicile means a permanent place of

abode, coupled with the intent to make the abode one's home. It is the

place that you intend to return to even if you visit or temporarily

reside elsewhere. Thus, actual presence in a location at any given

time is not necessarily determinative of a person's domicile. An indi-

[ 1 ] OTS-4743.9

This rule was adopted June 28, 2024 and becomes effective July 29, 2024. It may be used to

determine tax liability on and after the effective date, until the codified version is available from the code reviser's office.

vidual can have only one domicile at a time. A Washington domiciliary

who intends

to move at a future date is still considered domiciled in

Washington. See subsection (6)(c) of this rule for more details.

(d) Family. Family means the same as "member of the family" in

RCW 83.100.046. See RCW 82.87.070.

(e) Federal net long-term capital gain. Federal net long-term

capital gain means the net long-term capital gain reportable for fed-

eral income tax purposes determined as if I.R.C. §§ 55 through 59,

1400Z-1, and 1400Z-2 did not exist. See RCW 82.87.020. This informa-

tion is reported on Schedule D of the U.S. Individual Income Tax Re-

turn.

(f) Grantor trust. A grantor trust is any trust in which the

grantor or another person is treated as the owner of any portion of

the trust for federal income tax purposes under I.R.C. §§ 671–679.

"Grantor trust" also includes any nongrantor trust where the grantor's

transfer of assets to the trust is treated as an incomplete gift under

I.R.C. § 2511 and accompanying regulations, to the extent that gran-

tor's transfer of assets to the trust is treated as an incomplete

gift. The grantor of a nongrantor trust must include any long-term

capital gain or loss from the sale or exchange of a capital asset at-

tributable to the grantor's gift to the trust, to the extent such gift

is incomplete, in the calculation of that individual's adjusted capi-

tal gain, if such gain or loss is allocated to this state under RCW

82.87.100.

(g) Intangible personal property. Intangible personal property

means all personal property other than tangible personal property. For

example, software is intangible personal property.

(h) Internal Revenue Code/I.R.C. Internal Revenue Code or I.R.C.

means Title 26 U.S.C., i.e., the United States Internal Revenue Code

of 1986, as amended, as of July 25, 2021, or as of such subsequent

date as noted in this rule. See RCW 82.87.020.

(i) Long-term capital asset. Long-term capital asset means a cap-

ital asset held for more than one year. See RCW 82.87.020.

(j) Materially participated. Materially participated means an in-

dividual was involved in the operation of a business on a basis that

is regular, continuous, and substantial. Materially participated gen-

erally has the same meaning as the term "material participation," as

defined in I.R.C. § 469 and related treasury regulations, to the ex-

tent not inconsistent with the qualified family-owned small business

deduction provided in RCW 82.87.070.

(k) Nongrantor trust. A nongrantor trust is any trust other than

a grantor trust.

(l) Permanent place of abode; place of abode. A place of abode

means a fixed dwelling or home maintained by an individual for occu-

pancy. Permanency of a place of abode is determined by whether the

place of abode serves more than a temporary purpose. Occupancy of the

dwelling or home, ownership status, nature, characteristics, use,

names, or labels of a dwelling are considered, but are not conclusive

as to determining the permanency of a place of abode. For example, a

rental apartment that an individual lives in for the tax year is indi-

cative of a permanent place of abode, while a camp or vacation home

that is suitable and in fact used only for vacations is not indicative

of a permanent place of abode.

(m) Principally directed or managed within the state of Washing-

ton. Principally directed or managed within the state of Washington

means that an organization's activities are primarily directed, con-

trolled, and coordinated in Washington. An office location in Washing-

[ 2 ] OTS-4743.9

This rule was adopted June 28, 2024 and becomes effective July 29, 2024. It may be used to

determine tax liability on and after the effective date, until the codified version is available from the code reviser's office.

ton alone does not establish that the organization is principally di-

rected or

managed in Washington. For example, a Washington location is

insufficient for this purpose if the organization's activities are not

primarily directed, controlled, and coordinated from the Washington

location. Organizations may submit an affidavit to the department at-

testing that the organization is principally directed or managed in

Washington. The affidavit is available at the department website,

dor.wa.gov.

(n) Qualified organization. A qualified organization means an or-

ganization that is eligible to receive a charitable contribution as

defined in I.R.C. § 170(c), and is principally directed or managed

within the state of Washington. See RCW 82.87.080.

(o) Qualifying interest. Qualifying interest means an interest in

a business that meets one of the following characteristics:

(i) An interest as a proprietor in a business carried on as a

sole proprietorship;

(ii) An interest in a business if at least 50 percent of the

business is owned, directly or indirectly, by any combination of the

taxpayer or members of the taxpayer's family, or both; or

(iii) An interest in a business if at least 30 percent of the

business is owned, directly or indirectly, by any combination of the

taxpayer or members of the taxpayer's family, or both, and:

(A) At least 70 percent of the business is owned, directly or in-

directly, by members of two families; or

(B) At least 90 percent of the business is owned, directly or in-

directly, by members of three families.

(p) Real estate. Real estate means land and fixtures affixed to

land, and also includes used mobile homes, used park model trailers,

used floating homes, and improvements constructed upon leased land.

See RCW 82.87.020.

(q) Resident.

(i) Resident generally includes any individual who is domiciled

in Washington during the taxable year. However, the term does not in-

clude a Washington domiciliary if the domiciliary:

(A) Did not maintain a permanent place of abode in Washington at

any time during the entire taxable year;

(B) Maintained a permanent place of abode outside of Washington

during the entire taxable year; and

(C) Spent in the aggregate not more than 30 days of the taxable

year in Washington. See RCW 82.87.020.

(ii) Resident also includes any individual not domiciled in Wash-

ington during the taxable year if the individual maintained a place of

abode in Washington at any time during the taxable year and was physi-

cally present in Washington for more than 183 days during the taxable

year. See RCW 82.87.020. A day, for purposes of this definition, means

a calendar day or any portion of a calendar day.

(r) Tangible personal property. Tangible personal property means

personal property that can be seen, weighed, measured, felt, or

touched, but does not include steam, electricity, or electrical ener-

gy.

(s) Taxpayer. Taxpayer means an individual, i.e., a natural per-

son, subject to the capital gains excise tax. In this rule, the tax-

payer is also referred to as "you" and "your."

(t) Washington capital gains. Washington capital gains means an

individual's adjusted capital gain, as modified in RCW 82.87.060, for

each return filed under this chapter. See RCW 82.87.020 and subsection

[ 3 ] OTS-4743.9

This rule was adopted June 28, 2024 and becomes effective July 29, 2024. It may be used to

determine tax liability on and after the effective date, until the codified version is available from the code reviser's office.

(5) of this rule for information on the deductions provided in RCW

82.87.060.

(3) Tax imposed.

(a) The

measure of tax; adjustments to federal net long-term cap-

ital gain. The capital gains excise tax is imposed on the sale or ex-

change of long-term capital assets. The measure of the capital gains

excise tax is Washington capital gains. Generally, Washington capital

gains begins with the taxpayer's reportable federal net long-term cap-

ital gain, and this amount is then adjusted by certain statutory addi-

tions and subtractions to reach adjusted capital gain. For example,

these adjustments remove exempt transactions or those not allocated to

Washington from the taxable measure. Statutory deductions further mod-

ify adjusted capital gain to reach the taxpayer's Washington capital

gains figure.

If your Washington capital gains are less than zero for a taxable

year, no tax is due under this section, and you are not allowed to

carryover this amount for use in the calculation of your adjusted cap-

ital gain for any other taxable year.

To the extent that a loss carryforward is included in the calcu-

lation of your federal net long-term capital gain and that loss carry-

forward is directly attributable to losses from sales or exchanges al-

located to this state under RCW 82.87.100, the loss carryforward is

included in the calculation of your adjusted capital gain. However,

you may not include any losses carried back for federal income tax

purposes in the calculation of your adjusted capital gain for any tax-

able year. See RCW 82.87.040.

(i)

The

effective date of the tax. The capital gains excise tax

is imposed on the sale or exchange of capital assets on and after Jan-

uary 1, 2022. Sales or exchanges occurring before the January 1, 2022,

effective date of the tax, are not part of the taxable measure of the

capital gains excise tax. There are at least two situations affected

by this timing issue:

(A) Loss carryforwards prior to 2022. Although the measure of the

capital gains excise tax is federal net long-term capital gain, you

must add back any loss carryforwards from sales or exchanges of long-

term capital assets that occurred prior to January 1, 2022, in calcu-

lating adjusted capital gain to the extent such loss was included in

calculating federal net long-term capital gain because any pre-2022

loss arose from a sale or exchange prior to the effective date of the

capital gains excise tax. See subsection (2)(a) of this rule for the

definition of adjusted capital gain.

(B) Installment sales. Long-term capital gain recognized from an

installment sale, as defined in I.R.C. § 453, is not subject to capi-

tal gains excise tax if the sale occurred before January 1, 2022, even

if some installment payments occur on or after January 1, 2022. You

should remove any gain recognized from installment sales that occurred

prior to January 1, 2022, in calculating adjusted capital gain to the

extent such gain was included in calculating federal net long-term

capital gain. See subsection (2)(a) of this rule for the definition of

adjusted capital gain. If the installment sale occurred on or after

January 1, 2022, you must include the long-term capital gain in the

measure of the Washington capital gains excise tax in the same manner

as the gain is reportable for federal tax purposes.

(ii)

Sale or exchange of long-term capital assets.

The imposition

of the capital gains excise tax is conditioned on the sale or exchange

of a long-term capital asset. In other words, if you sell or exchange

a capital asset resulting in a long-term capital gain or loss, that

[ 4 ] OTS-4743.9

This rule was adopted June 28, 2024 and becomes effective July 29, 2024. It may be used to

determine tax liability on and after the effective date, until the codified version is available from the code reviser's office.

gain or loss is included in calculating your adjusted capital gain.

Alternatively, if you

have a long-term capital gain or loss that did

not arise from a sale or exchange, then that gain or loss is not in-

cluded in calculating your adjusted capital gain.

Example 1: Gifts.

Facts: In 2024, Jane received an old baseball card worth $30,000

from her brother, Jim, as a gift. Jim has no reportable federal net

long-term capital gain from this transaction or from any other source.

Result: Because the transaction results in no federal long-term

capital gain, Jim has no capital gains excise tax liability from the

gift.

Example 2: Expatriation.

Facts: In 2024, Zander properly had federal net long-term capital

gain in the amount of $500,000. A portion, $100,000, is long-term cap-

ital gain recognized under I.R.C. § 877A(a) because Zander is expatri-

ating.

Result: Long-term capital gain is recognized under I.R.C. §

877A(a) as a result of a deemed sale. Because $100,000 of Zander's

gain is not the result of a sale or exchange of a capital asset, that

portion is not included in Zander's measure of Washington capital

gains. He should subtract $100,000 from his federal net long-term cap-

ital gain when calculating his Washington capital gains.

Example 3: Maturity of bonds.

Facts: In 2024, Zora had federal net long-term capital gain in

the amount of $500,000. A portion, $100,000, is long-term capital gain

recognized under I.R.C. § 1271 upon the retirement of bonds Zora had

purchased at discount.

Result: Upon the retirement of the bonds, Zora receives cash and

no longer holds the capital assets (i.e., the bonds). These circum-

stances indicate the transaction is an exchange for purposes of the

capital gains excise tax, and Zora should include the long-term capi-

tal gain recognized from the bonds in her Washington capital gains

amount.

Example 4: Excess partnership distribution.

Facts: In 2024, Zane had federal net long-term capital gain in

the amount of $500,000. A portion, $100,000, is long-term capital gain

recognized under I.R.C. § 731 because the partnership in which Zane is

a partner distributed cash to him in an amount that exceeded Zane's

basis in the partnership.

Result: The long-term capital gain that Zane recognizes from the

excess distribution is not due to a sale or exchange of a capital as-

set. Therefore, Zane should subtract $100,000 from his federal net

long-term capital gain when calculating his Washington capital gains.

Example 5: Section 1256 contracts.

Facts: In 2023, Mavis, a Washington domiciliary, recognized both

gains and losses from various Section 1256 contracts, as defined in

I.R.C. § 1256. Mavis recognized a $300 gain from the sale of an 18-

month futures contract that she held for one year and three months, a

$400 loss from the sale of a three-month nonequity option contract

that she held for one month, and a $100 gain from a 24-month foreign

currency contract that she continues to hold, but was deemed sold at

the end of the year for federal tax purposes. Under I.R.C. § 1256, 60

percent of the gain or loss from Section 1256 contracts is treated as

long-term capital gain or loss, and 40 percent is treated as short-

[ 5 ] OTS-4743.9

This rule was adopted June 28, 2024 and becomes effective July 29, 2024. It may be used to

determine tax liability on and after the effective date, until the codified version is available from the code reviser's office.

term capital gain or loss. For federal tax purposes, Mavis had $0 in

net capital gain from these contracts for 2023.

Result: Although Mavis had $0 in federal net long-term capital

gain from

the Section 1256 contracts in 2023, only long-term capital

gains and losses from Section 1256 contracts that were held for more

than one year and were sold are included in calculating an individu-

al's Washington capital gains excise tax. Here, Mavis sold or ex-

changed only one contract that she held for more than one year, the

18-month contract. Therefore, Mavis should calculate her Washington

capital gains from her Section 1256 contracts by including only the

$180 in long-term capital gain she recognized from her sale of the 18-

month futures contract. The $240 long-term capital loss she recognized

for federal tax purposes on the three-month contract and the $60 long-

term capital gain she recognized on the 24-month contract are not part

of her Washington capital gains.

(iii) Other examples on the measure of tax.

Example 6: Capital gain invested in qualified opportunity fund.

Facts: In 2023, Joseph, a Washington domiciliary, sold stock he

had held for two years for $2,000,000. His basis in the stock was

$700,000. He invests in the same year, $1,300,000 in a qualified op-

portunity fund, as defined in I.R.C. § 1400Z-2, and elects to defer

federal taxation of the gain from the sale of his stock as permitted

under I.R.C. § 1400Z-2. Joseph sells no other capital assets in 2023.

As a result of the deferral, Joseph recognizes in 2023 $0 net long-

term capital gain for federal tax purposes.

Result: An individual's Washington capital gains is based on

their federal net long-term capital gain, which is defined as the net

long-term capital gain reportable for federal income tax purposes de-

termined as if Title 26 U.S.C. Secs. 55 through 59, 1400Z-1, and

1400Z-2 of the Internal Revenue Code did not exist. Because the defi-

nition of federal net long-term capital gain excludes Section 1400Z-2

of the Internal Revenue Code, Joseph must include the $1,300,000 in

long-term capital gain from his 2023 sale of stock in calculating his

2023 Washington capital gains.

Example 7: Sale of qualified opportunity fund.

Facts: Same facts as Example 6, and Joseph sells his investment

in the qualified opportunity fund in 2025 for $1,700,000. Under the

basis and gain recognition rules in I.R.C. § 1400Z-2, Joseph must rec-

ognize $1,300,000 in long-term capital gain on the sale of his inter-

est in the qualified opportunity fund for federal tax purposes.

Result: The definition of federal net long-term capital gain for

purposes of the Washington capital gains excise tax excludes Section

1400Z-2 of the Internal Revenue Code. Therefore, Joseph should ignore

I.R.C. § 1400Z-2 when calculating the gain from the sale of his quali-

fied opportunity fund investment for purposes of the Washington capi-

tal gains excise tax, and, in this case, calculate his gain or loss by

applying I.R.C. §§ 1001, 1011, and 1012.

Example 8: Section 1244 stock loss.

Facts: In 2023, David, who is domiciled in Washington, sold stock

he had held for several years. Some of the stock sold by David was

Section 1244 stock, as defined under I.R.C. § 1244(c). The sale of the

Section 1244 stock resulted in a $50,000 loss, which David properly

reported on his 2023 tax return as an ordinary loss. David's other

stock sales in 2023 resulted in a net long-term capital gain of

[ 6 ] OTS-4743.9

This rule was adopted June 28, 2024 and becomes effective July 29, 2024. It may be used to

determine tax liability on and after the effective date, until the codified version is available from the code reviser's office.

$1,300,000 and a net short-term capital loss of $20,000. David had no

other capital gains or losses.

Result: Neither the $50,000 ordinary loss nor the $20,000 short-

term capital

loss David reported on his 2023 federal tax return are

included in his federal net long-term capital gain. As a result, nei-

ther loss amount is included in calculating David's Washington capital

gains. David's 2023 Washington capital gains amount is his federal net

long-term capital gain, $1,300,000, subject to the exemptions and de-

ductions discussed in subsections (4) and (5) of this rule.

Example 9: Section 1061 applicable partnership interests.

Facts: Marcy owns interests in partnerships that are "applicable

partnership interests" under I.R.C § 1061. Marcy is a Washington domi-

ciliary. In 2023, she reports on her federal tax return $1,000,000 in

capital gain passed through from her partnerships, all from the sale

of intangible long-term capital assets. A portion of this capital

gain, $200,000, is recharacterized as short-term capital gain under

I.R.C. § 1061. She reports the remainder, $800,000, as long-term capi-

tal gain. Marcy has no other capital gain or losses in 2023.

Result: The $200,000 in capital gain that is recharacterized as

short-term capital gain under I.R.C. § 1061 is not part of Marcy's net

long-term capital gain reportable for federal income tax purposes.

Therefore, Marcy's 2023 Washington capital gains amount is $800,000,

subject to the exemptions and deductions discussed in subsections (4)

and (5) of this rule.

Example 10: Loss carried forward from a prior year.

Facts: In 2023, John incurs a $1,003,000 long-term capital loss

from a sale of stock while John was domiciled in Washington. John does

not have any capital gains against which he can apply the loss. Under

I.R.C. § 1211, $3,000 of the loss is applied against ordinary income

that John earned in 2023. Therefore, $1,000,000 of the loss is carried

forward to 2024 under I.R.C. § 1212. In 2024, John incurs a $4,000,000

long-term capital gain from sales of stock while John continues to be

domiciled in Washington. On John's federal return, John applies the

$1,000,000 loss from 2023 and reports a federal net long-term capital

gain of $3,000,000 for 2024.

Result: To calculate John's 2024 Washington capital gains, the

starting point is John's federal net long-term capital gain of

$3,000,000. None of the adjustments in RCW 82.87.020(1) apply in de-

termining John's adjusted capital gain. Therefore, John's 2024 Wash-

ington capital gains amount is $3,000,000, subject to the exemptions

and deductions discussed in subsections (4) and (5) of this rule.

Example 11: Out-of-state loss carried forward from a prior year.

Facts: Same facts as Example 10, except John incurs a net

$1,003,000 long-term capital loss from a sale of stock while John was

domiciled in Oregon, and John becomes domiciled in Washington in 2024.

Result: To calculate John's 2024 Washington capital gains, the

starting point is John's federal net long-term capital gain of

$3,000,000. RCW 82.87.020 (1)(c) instructs that the $1,000,000 loss

carryforward must be added back to the $3,000,000 federal net long-

term capital gain amount because all $1,000,000 of the loss was from a

sale or exchange that was not allocated to Washington. Therefore,

John's 2024 Washington capital gains amount is $4,000,000, subject to

the exemptions and deductions discussed in subsections (4) and (5) of

this rule.

Example 12: Short-term capital losses.

[ 7 ] OTS-4743.9

This rule was adopted June 28, 2024 and becomes effective July 29, 2024. It may be used to

determine tax liability on and after the effective date, until the codified version is available from the code reviser's office.

Facts: In 2023, Jason, a Washington domiciliary, realizes a

$403,000 short-term capital

loss from sales of securities, and a

$325,000 net long-term capital gain from a sale of investment proper-

ty. That year, he also earns $125,000 in other income. For federal tax

purposes, $3,000 of the short-term capital loss is applied against Ja-

son's other income and $325,000 of the short-term capital loss is ap-

plied against Jason's long-term capital gain. The remaining $75,000

net short-term capital loss is carried forward to 2024.

Result: Jason's 2023 Washington capital gains amount is his fed-

eral net long-term capital gain, $325,000, subject to the exemptions

and deductions discussed in subsections (4) and (5) of this rule.

Example 13: Short-term loss carried forward.

Facts: Same facts as Example 12, and in 2024, Jason realizes

long-term capital gain totaling $1,000,000, and short-term capital

gain totaling $200,000, all from sales of securities. For federal tax

purposes, the $75,000 short-term capital loss carried forward from

2023 is applied against Jason's 2024 $200,000 net short-term capital

gain.

Result: Jason's 2024 Washington capital gains amount is

$1,000,000, subject to the exemptions and deductions discussed in sub-

sections (4) and (5) of this rule.

(b)

Beneficial ownership;

pass-through entities. The capital

gains excise tax applies to the sale or exchange of long-term capital

assets owned by individuals. Ownership includes both legal and benefi-

cial ownership. An individual is considered to be a beneficial owner

of long-term capital assets held by any pass-through or disregarded

entity in which the individual holds an ownership interest, to the ex-

tent of the individual's ownership interest in the entity as reported

for federal income tax purposes. See RCW 82.87.040. Accordingly, you

must include both gains from the sale or exchange of capital assets of

which you are the legal owner and gains passed through to you from the

sale or exchange of capital assets of which you are a beneficial own-

er. Examples of pass-through entities for federal tax purposes include

partnerships, limited liability companies, S corporations, and grantor

trusts. See RCW 82.87.040. The department does not consider estates,

or trusts other than grantor trusts, to be pass-through entities. How-

ever, beneficiaries of estates and nongrantor trusts may nevertheless

be subject to capital gains excise tax on distributions of capital

gains received from estates and nongrantor trusts.

Example 14: Mutual fund.

Facts: Jane is domiciled in Washington and an investor in a mutu-

al fund. A mutual fund is formed as a regulated investment company, a

type of pass-through entity for federal income tax purposes. In 2024,

the fund earns long-term capital gain from the sale of capital assets

held by the fund. Some of the capital gain is distributed to the

fund's shareholders, and some of the gain is retained in the fund and

reported as undistributed capital gain.

Result: Jane is liable for capital gains excise tax on her Wash-

ington capital gains arising from the sale of the fund's long-term

capital assets to the extent of her ownership interest in the fund as

reported for federal income tax purposes, including her share of the

fund's undistributed capital gain, subject to the exemptions and de-

ductions discussed in subsections (4) and (5) of this rule.

Example 15: S corporation.

[ 8 ] OTS-4743.9

This rule was adopted June 28, 2024 and becomes effective July 29, 2024. It may be used to

determine tax liability on and after the effective date, until the codified version is available from the code reviser's office.

Facts: Jack is domiciled in Washington. He is a 50 percent share-

holder of

an S corporation. The S corporation is a long-time share-

holder of a C corporation. The S corporation sells the C corporation

shares, resulting in long-term capital gain, 50 percent of which is

passed through to Jack for federal income tax purposes.

Result: Jack is a beneficial owner of the S corporation's assets.

Jack must include his 50 percent share of the long-term capital gain

arising from the S corporation's sale of stock in calculating his

Washington capital gains.

Example 16: Tiered partnership – Limited liability company.

Facts: Juan is domiciled in Washington. Juan is a 50 percent own-

er of a partnership. The partnership is a 50 percent owner of an LLC.

The LLC sells an intangible asset that it has owned for two years,

which results in long-term capital gain. As the owner of the partner-

ship, 25 percent of the long-term capital gain from the LLC's sale of

the intangible asset is passed through to Juan for federal income tax

purposes.

Result: Because Juan is an owner of a pass-through entity, the

partnership, and the partnership is an owner of another pass-through

entity, the LLC, Juan is a beneficial owner of the LLC's assets.

Therefore, Juan must include in calculating his Washington capital

gains, the long-term capital gain passed through to him arising from

the LLC's sale of the intangible asset.

(4)

Exemptions. You

may treat certain types of sales or exchanges

as exempt from the capital gains excise tax. See RCW 82.87.050. These

exemptions are subject to the following guidelines.

(a)

Real

estate. Generally, long-term capital gains from sales or

exchanges of real estate are not subject to capital gains excise tax.

This exemption applies to all real estate transferred by deed, real

estate contract, judgment, or other lawful instruments that transfer

title to real property and are filed as a public record with the coun-

ties where real property is located.

Example 17: Sale of real estate by an individual.

Facts: Pamela is a Washington domiciliary and owns investment re-

al property in Western Washington. In 2025, a real estate developer

offers to buy the real property. Pamela accepts the developer's offer

and completes the sale the same year. The sale results in a

$10,000,000 long-term capital gain, which Pamela reports for federal

income tax purposes. Pamela's only other transaction in 2025 involving

long-term capital assets is a sale of some stock that resulted in

$300,000 in long-term capital gain. Her total federal net long-term

capital gain in 2025 is $10,300,000.

Result: Pamela is exempt from Washington capital gains excise tax

on the $10,000,000 long-term capital gain arising from the sale of the

real property. In calculating adjusted capital gain for 2025, Pamela

should subtract the $10,000,000 from her federal net long-term capital

gain as an amount of long-term capital gain from a sale or exchange

that is exempt under chapter 82.87 RCW. Pamela's 2025 Washington capi-

tal gains equals $300,000, subject to the exemptions and deductions

discussed in subsections (4) and (5) of this rule.

Example 18: Sale of real estate by pass-through entity.

Facts: Paul and Pierre each own 50 percent of Invesco LLC. Inves-

co owns 100 percent of two other LLCs, PropertyOne LLC and PropertyTwo

LLC. PropertyOne's only asset is investment real property located in

Eastern Washington. In 2024, PropertyOne sells the investment proper-

[ 9 ] OTS-4743.9

This rule was adopted June 28, 2024 and becomes effective July 29, 2024. It may be used to

determine tax liability on and after the effective date, until the codified version is available from the code reviser's office.

ty, resulting in $6,000,000 of long-term capital gain. For federal tax

purposes, Paul and

Pierre each recognize $3,000,000 in long-term capi-

tal gain from their distributive shares of the capital gain passed-

through from PropertyOne.

Result: PropertyOne's sale of the investment property is exempt

from capital gains excise tax. In calculating their Washington capital

gains, Paul and Pierre should each subtract the $3,000,000 from their

federal net long-term capital gain as an amount of long-term capital

gain from a sale or exchange that is exempt under chapter 82.87 RCW.

(b)

Sales of entities owning real estate.

The sale of an interest

in a privately held entity is exempt from the capital gains excise tax

to the extent the long-term gain or loss from the sale is directly at-

tributable to real estate owned directly by the entity.

(i) A "privately held entity" for this purpose means an entity

that is not traded through public means. For example, a privately held

entity does not include a corporation traded on a public exchange.

(ii) "Owned directly" means the privately held entity in which

the individual has an interest legally owns (holds legal title to) the

real estate.

(iii) The value of this exemption is equal to the fair market

value of the real estate owned directly by the privately held entity

less its basis at the time that the sale or exchange of the individu-

al's interest occurs, multiplied by the percentage of the ownership

interest in the entity that is sold or exchanged by the individual.

The following are not considered in the calculation of the exemption

amount:

(A) Any amount that I.R.C. § 751 treats as an amount realized

from the sale or exchange of property other than a capital asset; and

(B) Real estate not owned directly by the entity in which an in-

dividual is selling or exchanging the individual's interest.

(iv) The fair market value of real estate may be established by a

fair market value appraisal issued by a state-licensed real estate ap-

praiser or an allocation of assets by the seller and the buyer made

consistent with the principles required for an allocation under I.R.C.

§ 1060, as amended, and related treasury regulations. However, the de-

partment is not bound by the parties' agreement as to the allocation

of assets, allocation of consideration, or fair market value, if such

allocations or fair market value do not reflect the fair market value

of the real estate. The assessed value of the real estate for property

tax purposes may also be used to determine the fair market value of

the real estate if the assessed value is current as of the date of the

sale or exchange of the ownership interest in the entity owning the

real estate and the department determines that this method is reasona-

ble under the circumstances. In no case may the exemption value under

(b) of this subsection exceed the individual's long-term capital gain

from the sale or exchange of the interest in the entity for which the

individual is claiming this exemption.

Example 19: Sale of private entity directly and indirectly owning

real estate.

Facts: Ken, who is domiciled in Washington, owns 100 percent of

Holding Company LLC. Holding Company LLC owns three assets: A 100 per-

cent interest in First Avenue Tower LLC, a 100 percent interest in

Second Avenue Tower LLC., and 100 percent of Third Avenue Tower, a

commercial building. All of the entities are privately held entities.

First Avenue Tower LLC owns one asset: First Avenue Tower, a commer-

cial building with a fair market value of $4,000,000, and a basis of

[ 10 ] OTS-4743.9

This rule was adopted June 28, 2024 and becomes effective July 29, 2024. It may be used to

determine tax liability on and after the effective date, until the codified version is available from the code reviser's office.

$1,000,000. Second Avenue Tower LLC also owns only one asset, a com-

mercial building called

Second Avenue Tower. Second Avenue Tower has a

fair market value of $8,000,000, and a basis of $5,000,000. Third Ave-

nue Tower has a fair market value of $5,000,000, and a basis of

$2,000,000.

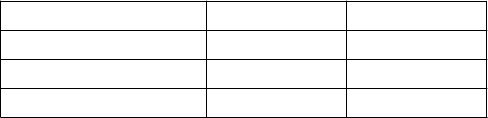

Real estate FMV Basis

First Avenue Tower $4,000,000 $1,000,000

Second Avenue Tower $8,000,000 $5,000,000

Third Avenue Tower $5,000,000 $2,000,000

Ken sells his entire interest in Holding Company LLC for

$17,000,000. His gain

from the sale is a $9,000,000 long-term capital

gain.

Result: A portion of the $9,000,000 gain Ken recognizes from the

sale of Holding Company LLC may qualify for exemption. Ken's long-term

capital gain from the sale of his Holding Company LLC interest is in-

eligible for the exemption with respect to First Avenue Tower and Sec-

ond Avenue Tower because Holding Company LLC does not directly own

those properties. However, Holding Company LLC owns Third Avenue Tower

directly. Therefore, $3,000,000 of Ken's gain from the sale of Holding

Company LLC is exempt. This amount is the difference between the fair

market value of Third Avenue Tower and the basis of that property.

Example 20: Sale of private entity directly and indirectly owning

real estate.

Facts: Same general facts as Example 19, except Holding Company

LLC liquidates First Avenue Tower LLC prior to Ken's sale of Holding

Company LLC. As a result of the liquidation, at the time of Ken's sale

of his Holding Company interest, Holding Company LLC directly owns the

commercial building previously held by First Avenue Tower LLC, as well

as Third Avenue Tower.

Result: A portion of the $9,000,000 gain Ken recognizes from the

sale of Holding Company LLC may qualify for exemption. Specifically,

the value of the exemption equals $6,000,000, which is the $4,000,000

fair market value of First Avenue Tower minus its $1,000,000 basis,

plus the $5,000,000 fair market value of Third Avenue Tower minus its

$2,000,000 basis, multiplied by Ken's 100 percent ownership interest

in Holding Company LLC.

Example 21: Sale of private entity directly owning a partial in-

terest in real estate.

Facts: Mitch is a Washington domiciliary who owns 100 percent of

Mitch Holdings LLC. Mitch Holdings LLC owns one asset, a 40 percent

interest in an investment property. Mitch recently decided to divest

from the property and did so by selling his entire interest in Mitch

Holdings LLC to another person. The assessed value of the investment

property is $2,300,000.

Result: Mitch Holdings LLC is a privately held entity. Mitch's

sale of Mitch Holdings LLC is exempt from the capital gains excise tax

to the extent the long-term gain or loss from the sale is directly at-

tributable to real estate owned directly by Mitch Holdings LLC, in

this case, the investment property. The value of the exemption for

Mitch is equal to the fair market value of Mitch Holdings LLC's inter-

est in the investment property, less its basis. Mitch should obtain an

appraisal to determine the fair market value of Mitch Holdings LLC's

interest in the property. See RCW 82.87.050. While the assessed value

of real estate may be used in some circumstances to determine fair

[ 11 ] OTS-4743.9

This rule was adopted June 28, 2024 and becomes effective July 29, 2024. It may be used to

determine tax liability on and after the effective date, until the codified version is available from the code reviser's office.

market value, use of assessed value, or a percentage of the assessed

value, is not

a reasonable method for determining the fair market val-

ue of a partial interest in real estate.

Example 22: Sale of private entity owning real estate; exemption

limitation.

Facts: Jesse, a Washington domiciliary, owns 100 percent of Prop-

erty Co., an LLC. Property Co. owns three assets: A 100 percent inter-

est in Property One LLC, a 100 percent interest in Property Two LLC,

and a piece of real estate, Property 3. Property One LLC's only asset

is real estate, Property 1, which has a fair market value of

$5,000,000, and a basis of $2,000,000. Property Two LLC's only asset

is a piece of depressed real estate, Property 2, which has a fair mar-

ket value of $2,000,000, and a basis of $10,000,000. Property 3 has a

fair market value of $12,000,000, and a basis of $5,000,000.

FMV Basis

Property 1 $5,000,000 $2,000,000

Property 2 $2,000,000 $10,000,000

Property 3 $12,000,000 $5,000,000

Jesse sells her entire interest in Property Co. for $19,000,000.

Jesse's basis in

Property Co. is $17,000,000. The sale results in a

$2,000,000 long-term capital gain for Jesse.

Result: The value of this exemption is equal to the fair market

value of the real estate owned directly by the privately held entity,

less its basis. However, the exemption value may not exceed the indi-

vidual's long-term capital gain or loss from the sale or exchange of

the interest in the entity. Here, Property 3 is the only real estate

owned directly by Property Co. Its fair market value minus its basis

is $7,000,000. However, Jesse's gain from the sale of Property Co. is

only $2,000,000. Therefore, the value of the exemption from Jesse's

sale of Property Co. is limited to $2,000,000.

(c)

Retirement accounts.

Sales or exchanges of assets held under

retirement savings accounts or retirement savings vehicles that are

exempt from federal income tax are also generally exempt from capital

gains excise tax. Exempt retirement accounts include the following:

(i) Retirement savings accounts under I.R.C. § 401(k);

(ii) Tax-sheltered annuities or custodial accounts described in

I.R.C. § 403(b);

(iii) Deferred compensation plans under I.R.C. § 457(b);

(iv) Individual retirement accounts or individual retirement an-

nuities described in I.R.C. § 408;

(v) Roth individual retirement accounts described in I.R.C. §

408A;

(vi) Employee defined contribution programs, employee defined

benefit plans; and

(vii) Retirement savings vehicles or accounts similar to those

described above, such as exempt foreign retirement accounts.

(d)

Assets

subject to condemnation. Sales or exchange of assets

pursuant to, or under imminent threat of condemnation proceedings by

the United States, the state or any of its political subdivisions, or

a municipal corporation, are exempt from capital gains excise tax.

(e)

Certain livestock.

Sales or exchanges of cattle, horses, or

breeding livestock are exempt if, for the taxable year of the sale or

exchange, more than 50 percent of the taxpayer's gross income for the

[ 12 ] OTS-4743.9

This rule was adopted June 28, 2024 and becomes effective July 29, 2024. It may be used to

determine tax liability on and after the effective date, until the codified version is available from the code reviser's office.

taxable year, including from the sale or exchange of capital assets,

is from farming or ranching.

(f) Depreciable property. Sales or exchanges of property that is

depreciable under I.R.C.

§ 167(a)(1) or that qualifies for expensing

under I.R.C. § 179 is exempt from capital gains excise tax. Intangi-

bles amortizable under I.R.C. § 197 do not qualify for this exemption.

Example 23: Nondepreciable intangible property.

Facts: Bob, a Washington domiciliary, sells in 2023 all his as-

sets in a Burger Bob franchise store that he acquired in 2018. The

sale results in long-term capital gain. A portion of the long-term

capital gain was attributable to Bob's sale of goodwill in the store.

Bob claims an exemption from capital gains excise tax on the portion

of the long-term capital gain that is attributable to goodwill.

Result: Bob's long-term capital gain from the sale of the good-

will is not exempt from capital gains excise tax because goodwill is

an intangible amortizable under I.R.C. § 197 rather than property de-

preciable under I.R.C. § 167(a)(1) or property that qualifies for ex-

pensing under § 179.

(g)

Timber and

timberland. Sales of timber as defined in RCW

82.87.050, and timberland, as well as capital gains received as divi-

dends and distributions from real estate investment trusts derived

from gains from the sale or exchange of timber and timberland, are ex-

empt from capital gains excise tax. Cutting or disposal of timber

qualifying for capital gains treatment under I.R.C. § 631(a) or (b) is

also considered a sale or exchange that is exempt from capital gains

excise tax.

(h)

Commercial fishing

privileges. Sales or exchanges of commer-

cial fishing privileges, as defined in RCW 82.87.050, are exempt from

capital gains excise tax.

(i)

Goodwill

in an auto dealership. Sales or exchanges of good-

will received from the sale of an auto dealership licensed under chap-

ter 46.70 RCW whose activities are subject to chapter 46.96 RCW are

exempt from capital gains excise tax. However, long-term capital gain

from sales or exchanges of goodwill in other types of businesses are

not exempt from capital gains excise tax.

(5)

Deductions.

To obtain your Washington capital gains, you may

deduct certain amounts from the measure of your adjusted capital gain,

subject to the following guidelines. RCW 82.87.060.

(a) Standard deduction.

(i) Individuals other than spouses or state-registered domestic

partners are entitled to deduct $250,000 from their Washington capital

gains.

(ii) Spouses and state-registered domestic partners are limited

to a total standard deduction of $250,000, regardless of whether they

file joint or separate returns. In the case of spouses or domestic

partners filing separate returns, the deduction may be split in what-

ever manner the spouses or partners choose, so long as the total

claimed deduction does not exceed $250,000.

(b)

Charitable

donation deduction. A taxpayer may take a deduc-

tion from their Washington capital gains for certain charitable dona-

tions to one or more qualified organizations during a tax year. See

subsection (2) of this rule for "qualified organization" definition.

(i)

Deduction

amount; limitation. The charitable donation deduc-

tion equals the difference between the taxpayer's total qualifying

donations minus $250,000. The maximum charitable donation deduction in

a year is $100,000 per tax return, regardless of the taxpayer's filing

[ 13 ] OTS-4743.9

This rule was adopted June 28, 2024 and becomes effective July 29, 2024. It may be used to

determine tax liability on and after the effective date, until the codified version is available from the code reviser's office.

status. Thus, in the case of one joint tax return, the maximum chari-

table donation deduction

is $100,000 although the return is filed by

two individuals.

(ii)

Donor-advised funds;

indirect donations through intermedia-

ries. Generally, a donor-advised fund is a separately identified ac-

count that is maintained and operated by a nonprofit organization, and

each account is composed of donations that are made by individual do-

nors. Although the nonprofit organization has legal control over it,

individual donors maintain advisory privileges with respect to the

distribution of funds and management of the account's assets. If you

donate to a donor-advised fund or a similar intermediary charitable

vehicle, that intermediary, or in case of a donor advised fund, the

organization that owns or controls the fund, must qualify as a quali-

fied organization under RCW 82.87.080. The organization to which you

make the donation, and not the organization where the donation ends

up, determines whether you donated to a qualified organization.

Example 24: Qualifying charitable donations by a couple.

Facts: Chris and Hannah are a married couple. They file a joint

return for federal tax purposes, and therefore also file a joint capi-

tal gains excise tax return. See RCW 82.87.120. However, they maintain

some separate funds consisting of separate property (rather than com-

munity property). In 2024, each spouse made charitable donations to

qualified organizations using their separate funds. Chris made dona-

tions totaling $290,000, and Hannah made donations totaling $400,000.

Result: The maximum charitable donation deduction in a year is

$100,000 per tax return. Thus, the total charitable donation deduction

the couple can take on their joint capital gains excise tax return is

$100,000, even though the sum of the spouses' donations exceeded

$250,000 by more than $100,000.

Example 25: Nonqualifying charitable donation.

Facts: Jimmy donates $350,000 to the Global Wildlife Fund (GWF)

every year. GWF is an international nonprofit organization that aims

to conserve endangered species. Its global headquarters is in Sweden.

GWF has a U.S. headquarters in Washington, D.C., and has no presence

in Washington state. Jimmy claims a $100,000 charitable donation de-

duction on his capital gains excise tax return.

Result: The facts indicate that GWF is not principally directed

or managed within Washington state. Therefore, Jimmy is not eligible

for the charitable donation deduction for his donation to GWF, because

GWF is not a qualified organization under RCW 82.87.080.

(c)

Qualified

family-owned small business deduction. You may de-

duct the amount of adjusted capital gain derived in the taxable year

from your sale or transfer of a qualified family-owned small business,

subject to all the following requirements. RCW 82.87.070.

(i) The sale or transfer must be a sale of substantially all the

business's assets or a transfer of substantially all of your interest

in the business. A transfer of substantially all the business's as-

sets, means a sale of at least 90 percent of the business's real prop-

erty and tangible and intangible personal property, measured by fair

market value. A sale of substantially all of your interest in the

business, means a transfer of at least 90 percent of your interest in

the business.

(ii) You must have held a qualifying interest in the qualified

family-owned small business for at least five years immediately pre-

ceding the sale or transfer. A mere change in form of the business,

[ 14 ] OTS-4743.9

This rule was adopted June 28, 2024 and becomes effective July 29, 2024. It may be used to

determine tax liability on and after the effective date, until the codified version is available from the code reviser's office.

i.e., where no change in beneficial ownership of the business has oc-

curred, including no

change in the proportion of beneficial ownership

in the business, does not interrupt this required holding period.

(iii) You, or your family, or both, must have materially partici-

pated in operating the business for at least five of the 10 years im-

mediately preceding the sale or transfer, unless the sale or transfer

was to a member of your family. A mere change in form of the business,

i.e., where no change in beneficial ownership of the business has oc-

curred, including no change in the proportion of beneficial ownership

in the business, does not interrupt this required participation peri-

od.

(iv) The business's worldwide gross revenue cannot have exceeded

$10,000,000 in the 12-month period immediately preceding the sale or

transfer.

(6)

Allocation of

long-term capital gains and losses. Allocation

is the method for determining which long-term capital gains and losses

to include in computing a taxpayer's Washington capital gains.

(a)

Tangible personal

property. You must allocate to Washington

long-term capital gain or loss from a sale of tangible personal prop-

erty in two situations:

(i) The tangible personal property was located in Washington at

the time of the sale or exchange, i.e., the tangible personal property

was physically present in Washington at the time the sale or exchange

occurred; or

(ii) The tangible personal property was not located in Washington

at the time of the sale or exchange, but the transaction had each of

the following characteristics:

(A) The property was located in Washington at any time during the

year in which the sale or exchange occurred or in the immediately pre-

ceding year;

(B) The taxpayer was a Washington resident at the time the sale

or exchange occurred; and

(C) The taxpayer was not subject to the payment of an income or

excise tax legally imposed on the long-term capital gain by another

taxing jurisdiction. If the sale generated a loss, this element is met

if the loss is not included in the taxpayer's income or excise tax

base in another taxing jurisdiction. RCW 82.87.100.

Example 26: Allocation of gain from tangible personal property.

Facts: Michael is domiciled in Washington. His home is in Seat-

tle, and he resides there year-round. In October 2024, Michael decides

to sell a coin collection he inherited two years ago. In December, Mi-

chael brings the coins to Nevada, which does not have an income tax

and does not impose excise taxes on occasional sales. While in Nevada,

Michael sells the coin collection and the sale results in a $100,000

long-term capital gain.

Result: Michael's $100,000 long-term capital gain from the sale

is allocated to Washington for purposes of the capital gains excise

tax. Although he sold the coins in Nevada, they were located in Wash-

ington during the year in which the sale occurred, Michael was a Wash-

ington resident at the time the sale occurred, and Michael was not

subject to an income or excise tax on the sale of the coins in another

taxing jurisdiction.

(b)

Intangible personal

property. You must allocate to Washington

long-term capital gain or loss from a sale or exchange of intangible

personal property if you were domiciled in Washington at the time the

sale or exchange occurred. RCW 82.87.100.

[ 15 ] OTS-4743.9

This rule was adopted June 28, 2024 and becomes effective July 29, 2024. It may be used to

determine tax liability on and after the effective date, until the codified version is available from the code reviser's office.

(c) Determinations of domicile.

(i) Determination of intent, burden of proof. An intention to

make

a place of abode one's domicile is determined by facts and cir-

cumstances on a case-by-case basis. The department will review the

factors and some may be given more weight than others depending on the

facts and circumstances. The following is a nonexclusive list of fac-

tors the department will consider in evaluating an individual's domi-

cile:

• Length of time spent in a location;

• Expressed intent;

• Place of business, profession, or employment;

• Location of bank accounts;

• Residence and address for federal income and state tax purpo-

ses;

• Sites of personal and real property owned by the individual;

• State of motor vehicle and other personal property registra-

tion;

• State of motor vehicle driver's license;

• Location of schools attended by children;

• State of voter registration;

• Location of professional or business licenses;

• Payment of in-state tuition;

• Location from where financial transactions originate;

• Claiming of residence in a state for purposes of obtaining a

hunting or fishing license, eligibility to hold public office, eligi-

bility for obtaining a property tax benefit (such as a homestead ex-

emption), or for judicial actions;

• Mailing address.

Individuals may submit to the department a request for a ruling

on where the department considers individuals to be domiciled for pur-

poses of this tax.

(ii) Continuation and change of domicile. Your domicile, once es-

tablished, is presumed to continue. Therefore, if you have been domi-

ciled in Washington, you will have the burden of proving your domicile

has changed to a location outside of Washington. To establish a new

domicile, you must be physically present at the new place of intended

domicile and have an intention to make that new place your permanent

home. This means that, for instance, selling your former home or ac-

quiring a new one is not conclusive in establishing domicile.

(iii) Domicile of spouses, state-registered domestic partners,

children. The department will presume that the domicile of spouses or

state-registered domestic partners are the same. The department will

also presume that a child's domicile is the same as the domicile of

the child's parents until the child is no longer dependent and estab-

lishes his or her own separate domicile. If the parents have separate

domiciles, the department will presume that the domicile of the child

is the domicile of the parent with whom the child spends more time in

the tax year.

(iv) Exceptions. Federal law may apply to service members in de-

termination of domicile. Generally, under Title 50 U.S.C. § 571 (resi-

dence for tax purposes under the Servicemembers' Civil Relief Act), a

member of the armed forces does not acquire a new domicile solely be-

cause that individual was stationed elsewhere during a period of ac-

tive duty.

(d)

Credit for

taxes paid to other taxing jurisdictions. Taxpay-

ers may be entitled to a credit against capital gains excise tax equal

to the amount of any legally imposed income or excise tax paid by the

[ 16 ] OTS-4743.9

This rule was adopted June 28, 2024 and becomes effective July 29, 2024. It may be used to

determine tax liability on and after the effective date, until the codified version is available from the code reviser's office.

taxpayer to another taxing jurisdiction on capital gains derived from

capital assets within

the other taxing jurisdiction. See RCW

82.87.100. In no case may the credit under this subsection (c) exceed

the individual's capital gains excise tax liability on the capital as-

sets for the tax year in which the individual claims this credit. En-

titlement to this credit requires the following:

(i) Another taxing jurisdiction legally imposed an income or ex-

cise tax on capital gain included in the taxpayer's Washington capital

gains;

(ii) The taxpayer in fact paid the tax imposed by the other tax-

ing jurisdiction before the taxpayer filed their Washington capital

gains excise tax return on which the credit is claimed; and

(iii) The gain taxed by the other jurisdiction arose from the

sale or exchange of a capital asset within the other taxing jurisdic-

tion. For this purpose, the department will presume that long-term

capital gain from sales or exchanges of intangible personal property

are within the other taxing jurisdiction if the other taxing jurisdic-

tion legally imposed tax on the long-term capital gain derived from

the sale or exchange of the intangible personal property.

Example 27: Allocation of gain from intangible property and cred-

it for other taxes paid.

Facts: Julie is a Washington domiciliary and owns a second home

in New York. During 2025, she resided in New York for eight months and

in Washington the other four months. Julie is a casual investor. In

2025, Julie sold her investment in cryptocurrency to online buyers.

The sale generated long-term capital gain for Julie. Under New York

law, Julie is treated as a statutory resident even though she was do-

miciled in Washington. As a statutory resident, Julie is required to

remit to New York income tax on the income she earned from the sale of

the cryptocurrency. Julie pays the New York tax and files a Washington

capital gains excise tax return, claiming a credit for the income tax

paid to New York on the sale of the cryptocurrency.

Result: Because Julie was domiciled in Washington at the time the

sale or exchange occurred, the gain from her sale is allocated to

Washington. However, because New York legally imposed income tax on

Julie's sale of cryptocurrency and Julie remitted income tax on the

sale to New York, Julie is entitled to a credit against Washington

capital gains excise tax equal to the New York tax Julie paid on the

transaction.

(e)

Allocation

and sourcing of gains or losses from pass-through

entities. The allocation method for gains and losses is the same

whether you owned the property directly or indirectly through a pass-

through or disregarded entity.

Example 28: Allocation of passed through gain from intangible

property.

Facts: Jack is domiciled in Washington. He is a 50 percent share-

holder of Invest Corp., an S corporation. Invest Corp. is a long-time

shareholder of Fictional Co. In 2025, Invest Corp. sells its Fictional

Co. shares, resulting in long-term capital gain, 50 percent of which

is passed through to Jack for federal income tax purposes.

Result: The long-term capital gain from the sale of the Fictional

Co. stock is allocated to Washington because the stock is intangible

personal property and the taxpayer, Jack, was domiciled in Washington

at the time the sale occurred.

[ 17 ] OTS-4743.9

This rule was adopted June 28, 2024 and becomes effective July 29, 2024. It may be used to

determine tax liability on and after the effective date, until the codified version is available from the code reviser's office.